When I entered this business 40 years ago, it seemed reasonable to me to study how the best investors behaved. The two investing masters that I respected the most were Peter Lynch and Warren Buffett. If I was going to be of value to others, it only made sense that I learn as much as I could from those who had amassed the best and most consistent track records. What struck me the most, as I studied these Masters, was how similar and aligned their investment philosophies were.

Therefore, I concluded that there must be profound wisdom in their investing approaches and practices.

Today, some 40 years later, what frustrates me the most, is how so much of their words of wisdom go unheeded by investors. I feel that a lot of this has to do with most people’s almost uncontrollable need for instant gratification. The phrase ”active portfolio management” has taken on a new meaning in modern times. Today people think in terms of holding periods of days, weeks or months. Yet, two foundational principles shared by both Warren Buffett and Peter Lynch are to invest in great businesses for the long-term, and to ignore the stock market.

Wisdom of the Masters

Wisdom of the Masters

The following three quotes by Warren Buffett speak to these points:

"If you aren't willing to own a stock for 10 years don't even think about owning it for 10 minutes" Warren Buffett, 1996 Berkshire Hathaway annual report

"Inactivity strikes us as intelligent behavior." Warren Buffett, 1996 Berkshire Hathaway annual report

"I never attempt to make money on the stock market. I buy on the assumption that they could close the market the next day and not reopen it for five years." Warren Buffett

From Peter Lynch, we offer the following corroborative quote from his best-selling book One Up on Wall Street:

"The stock market ought to be irrelevant. If I could convince you of this one thing, I’d feel this book has done its job. If you don't believe me, believe Warren Buffett. "As far as I'm concerned," Buffett has written, "the stock market doesn't exist. It is only there is a reference to see if anybody is offering to do anything foolish."

Dividend Aristocrats - Validating the Wisdom of the Masters

In this article, our third in our series on how to know when to buy and when to sell a stock, we intend to test some of the important axioms promulgated by the investing greats Peter Lynch and Warren Buffett. We will endeavor to accomplish this by offering real-world examples as evidence of the veracity of their ideas. Our goal is not only to illuminate the lessons that these great investors have taught, but also to have a little fun along the way. In order to accomplish this, we will quote a lesson and then utilize our EDMP, Inc. F.A.S.T. Graphs™ to analyze dividend aristocrats that provide proof of the wisdom behind their words.

GDF-EDMP Value Formula for Moderate Growth

Before we get started some points of clarification regarding our EDMP, Inc. F.A.S.T. Graphs™ are in order. With the exception of one company in this article, Consolidated Edison (ED), the dividend aristocrats we will analyze will possess earnings growth rates between 5% and 15% (of course as dividend aristocrats, each will have a history of increasing their dividend for at least 25 consecutive years).

Therefore, each F.A.S.T. Graph™ will utilize our “GDF-EDMP” formula for valuing a moderately fast growing business. This formula is a modified version of Ben Graham's famous formula for valuing a business (best applied to low growth 5% or less) and the widely accepted PEG ratio formula (best applied to fast growers 15% or higher). Calculations based on these formulas will draw our orange earnings justified valuation line.

The essence of what the orange earnings justified valuation line represents is what we call earnings yield. This is the rate of return that the cash flows (earnings) of the business generates, based on the original capital investment into the business. In other words, this is the cash on cash return from the earnings the company produces. The slope of the line will equal the rate of change of earnings growth that the company produces over time. Therefore, if the stock price touches the orange line at the time of original investment and then touches it again at the ending date being measured, then the capital appreciation rate of return component will equal the growth rate of earnings.

To state this more simply, the thesis states that when the price touches the orange line the company is trading at fair value. When the price is above the orange line the stock is overpriced, and when the price is below the orange line the company is undervalued. However, in time the price will inevitably revert to the mean. Therefore, our F.A.S.T. Graph™ tool allows the researcher to visually determine whether the company is fairly priced, overpriced or under priced. In his best-selling book One Up on Wall Street, Peter Lynch had this to say about the relationship between a company's stock price and its earnings:

The Importance of Earnings "You can see the importance of earnings on any chart that has an earnings line running alongside the stock price. On chart after chart the two lines will move in tandem, or if the stock price strays away from the earnings line, sooner or later it will come back to the earnings." Peter Lynch - One Up On Wall Street

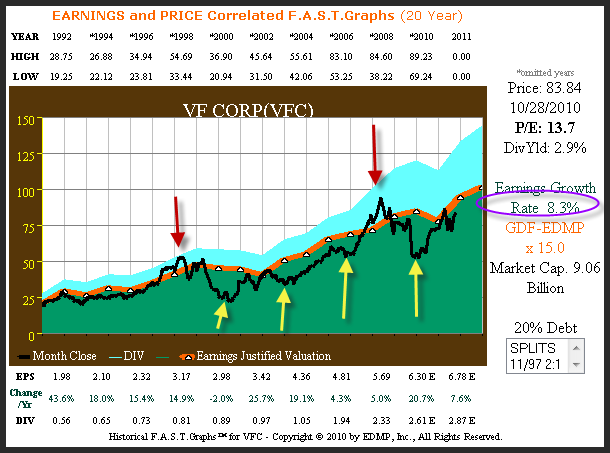

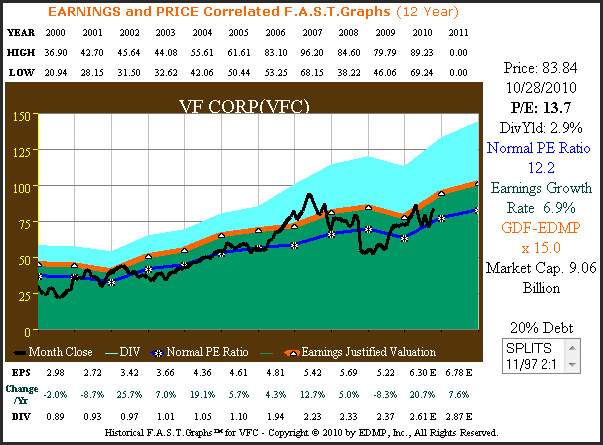

The following F.A.S.T. Graph™ on the VF Corp (VFC), a global apparel company, provides a quintessential example of Peter Lynch's words. As you can clearly see, the black price line follows the orange earnings justified valuation line very closely since 1992. When the price rises above the orange earnings justified valuation line, like it did in 1997 and 1998, it quickly came back to earnings. Then, it did this again in calendar year 2007 when the price of VF Corp. (VFC) once again became overvalued. Additionally, there were several periods where the price line fell below the orange earnings justified valuation line and then subsequently moved back to True Worth™ value. (Red arrows point to overvaluation – yellow arrows point to undervaluation).

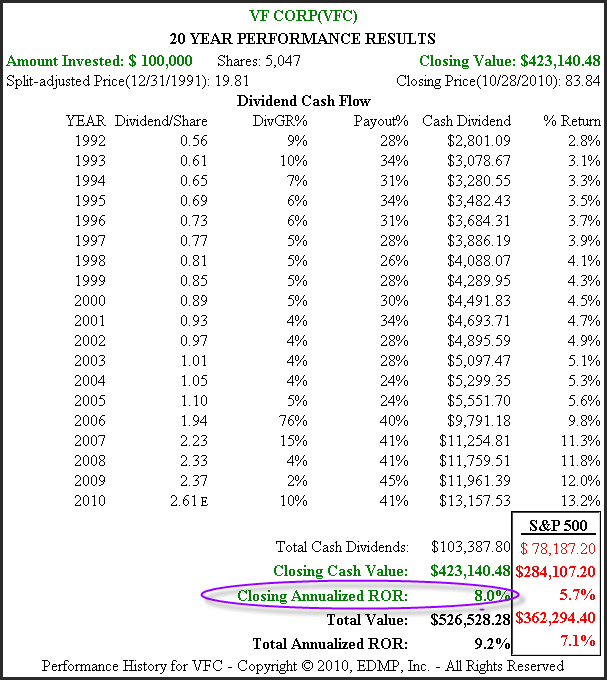

The following calculated performance chart associated with the above price and earnings correlated graph reveals the veracity of the relationship between earnings growth and shareholder returns. As can be seen from the above F.A.S.T. Graph™ of VF Corp. (VFC), the company's earnings growth rate was 8.3% (purple circle). The closing annualized rate of return of 8% (purple circle) shown on the chart below closely correlates to the earnings growth rate. Furthermore, this dividend aristocrat has generated a total return for its shareholders of 9.2%.

There are two points of interest that need to be noted here. First of all, VF Corp. (VFC) based on its starting fair valuation on 12/31/1991 and its earnings growth rate generated $323.140.48 of capital appreciation ($423,140.48 minus $100,000 originally invested). Secondly, dividend income of $103,387.80 represented about one third of the total return shareholders received. Clearly, capital gains (appreciation) were more important to shareholders from this moderately fast growing business.

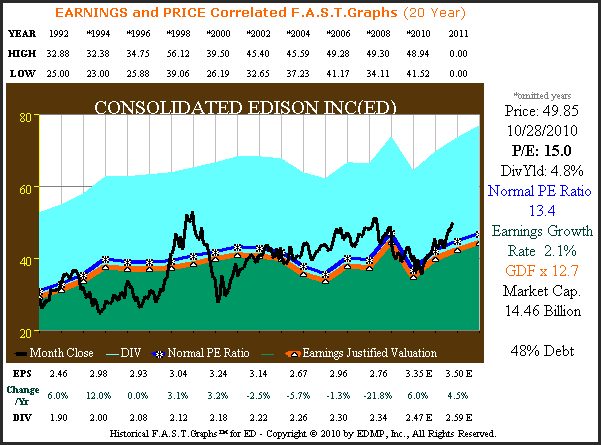

The F.A.S.T. Graph™ below revisits Consolidated Edison Inc. (ED), a slow-growing utility stock that we originally reviewed in our previous article in this series. Note that this earnings and price correlated F.A.S.T. Graph™ utilizes the GDF (Graham Dodd Formula) version for companies growing at 5% or less. However, also notice the validation of Peter Lynch's quote regarding the relationship of price-to-earnings. When the price line strays from the earnings justified valuation line, over or under, it inevitably returns to value.

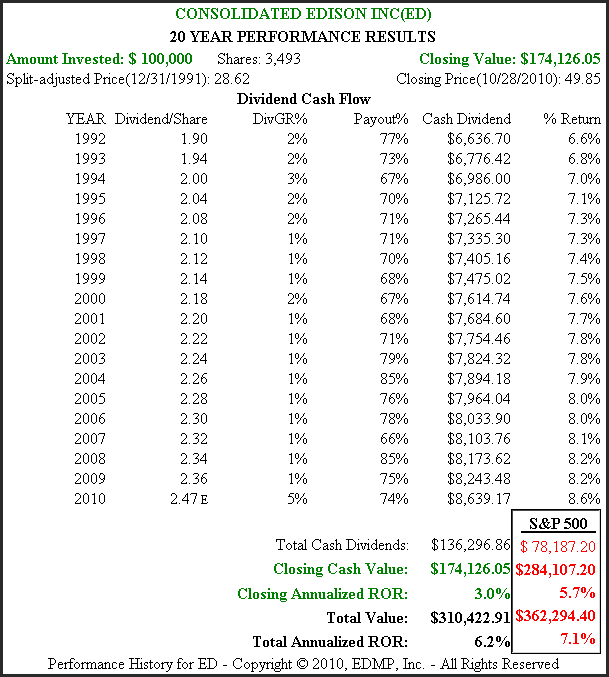

From the performance chart associated with earnings and price correlated F.A.S.T. Graphs™ above on Consolidated Edison Inc. (ED) there are a couple of important points to note. First of all, the closing annualized rate of return of 3% correlates very closely to the earnings growth of 2.1% seen in the graph above. Second, the dividend of $136,296.86 is greater than the $74,126.05 capital gain ($174,126.05 minus $100,000 originally invested equals $74,126.05). This establishes the fact that dividend income is much more important with slower growers than it is with moderate or fast growers.

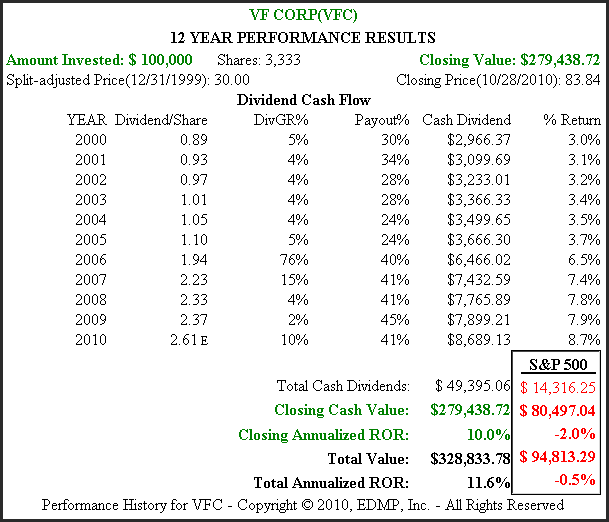

There is a second, but related Peter Lynch quote from his best-selling book One Up on Wall Street, that can be validated by looking at a second F.A.S.T. Graph™ on VF Corp. (VFC) over a timeframe which started with VF Corp. (VFC) being undervalued. The following F.A.S.T. Graph™ looks at VF Corp. (VFC) since calendar year 2000 when its price was below its earnings justified valuation line. Although its earnings growth rate had dropped from over 8% to just under 7%, you will soon discover from the associated performance graph below how undervaluation enhanced shareholder returns. But first, the Peter Lynch quote:

“A quick way to tell if a stock is overpriced is to compare the price line to the earnings line. If you bought familiar growth companies… when the stock price fell well below the earnings line, and sold them when the stock price rose dramatically about it, the chances are you'd do pretty well." Peter Lynch One Up On Wall Street

Although the above earnings and price correlated F.A.S.T. Graph™ does not end with the price dramatically above the earnings justified valuation line, it is clear from the associated performance chart below, that shareholder returns were enhanced to a level greater than the earnings growth rate achieved.

Undervaluation at the beginning of calendar year 2002 created a closing annualized rate of return of 10%, which was significantly greater than the 6.9% earnings growth rate achieved. When dividend income of $49,395.06 is added to the total (paid out not reinvested), the total annualized rate of return exceeds 11% per annum. As Peter Lynch stated, when you buy a great business on sale chances are you'll do pretty well.

More Important Lessons From the Masters

The following Warren Buffett and Peter Lynch quotes provide added color and insight into successfully answering the important questions of when to buy and when to sell a common stock. After each quote we will provide a link to a series of EDMP, Inc. F.A.S.T. Graphs™ that validate the primary message behind each of these words of wisdom from the masters. There will be a drop-down window at the top left of each quote where you can advance from the current graph to the next. A brief commentary explaining the points will be included.

"I don't believe in predicting markets. I believe in buying great businesses - especially companies that are undervalued, and/or under-appreciated" Peter Lynch One Up On Wall Street

{kind=link}

"What makes stocks valuable in the long run isn't the market. It's the profitability of the shares in the companies you own. As corporate profits increase, corporations become more valuable and sooner or later, their shares will sell for a higher price." Peter Lynch, Worth Magazine, September 1995

{kind=link}

"To buy excellent businesses at a price that makes business sense... this offers you the highest predictable annual compounding rate of return possible with the least amount of risk." Mary Buffett & David Clark 'Buffettology'

{kind=link}

"If we find a company we like, the level of the market will not really impact our decisions. We will decide company by company. We spend essentially no time thinking about macroeconomic factors. In other words, if somebody handed us a prediction by the most revered intellectual on the subject, with figures for unemployment or interest rates, or whatever it might be for the next two years, we would not pay any attention to it. We simply try to focus on businesses that we think we understand and where we like the price and management." Warren Buffett

{kind=link}

“To invest successfully over a lifetime does not require a stratospheric IQ, unusual business insights or inside information. What's needed is a sound intellectual framework for making decisions and the ability to keep emotions from corroding that framework." Warren Buffett

{kind=link}

With all due humility and reverence to the masters quoted in this article, I offer the following quote from yours truly, that summarizes the important messages contained in this article.

"In the long run, it's EARNINGS that determine market price and dividend income."Charles C. Carnevale, EDMP, Inc.

{kind=link}

Summary and Conclusions

When you carefully scrutinize the important messages and lessons taught by great masters like Warren Buffett and Peter Lynch, you should be convinced of the wisdom of their words. Most of what they teach can be validated and seen in real world examples with real world companies. We offered many examples in this article to substantiate these statements.

In the long run the evidence seems clear, earnings determine market price and dividend income. Both your expected capital appreciation and total dividend income will be a function of earnings and how fast earnings grow. Valuation, or more importantly, sound valuation is a key to achieving the appropriate returns from any given company relative to its specific rate of change of earnings growth. Once you understand these critical relationships between earnings and valuation and how they relate to stock prices and dividends, sound and safe investing decisions can be intelligently made. In our next series we will look at when to buy or sell REITs and MLPs.

No comments:

Post a Comment